Introduction

The reformation of The Indonesian Health System that became National Health Insurance (NHI) by using capitation method made a significant change in basic healthcare services. Capitation method is influenced by utilisation and unit cost calculation. Puskesmas, that stand for Community-based health service, is a primary healthcare full financed by Indonesian government capitation and focus on free simple healthcare. Inequalities of puskesmas distribution spread all over Indonesia, including in urban and rural area and impacted the oral health outcome and dental service delivery.

Aim

To calculate and to analyse the comparison of dental service-unit cost value after the reformation of Indonesian NHI at the urban and rural puskesmas in Padang City, Indonesia.

Materials and Methods

Two of 22 total puskesmas were chosen by random sampling, one puskesmas was representative for urban and rural counterpart. The data was collected, extracted and analysed. Then two administrative officers where interviewed, at each puskesmas. The Activity Based Costing (ABC) method was used to calculate the unit cost of dental healthcare services.

Results

Unit cost of dental service in urban puskesmas was IDR 86,652, and rural was IDR 108,721. Rural puskesmas has high total cost and low activity driver. On the other hand, low total cost with high activity driver was found at urban puskesmas.

Conclusion

Rural puskesmas has higher unit cost value than urban puskesmas. Hence, it may help the Indonesian government to distribute equal capitation expenditure on dental service at each puskesmas in Indonesia.

Cost, Healthcare, National health insurance

Introduction

Since January 1, 2014, the Indonesian government has implemented the National Health Insurance System (NHI) under Act No. 24 of 2011 managed by the Social Security Administering Board/Badan Penyelenggara Jaminan Sosial (BPJS) [1,2]. Puskesmas, stand for community-based health service, was designed by the Indonesian government [3,4]. As a primary health centre, puskesmas are spread over 33 provinces in Indonesia. Estimated 30,000 puskesmas are distributed in entire province and sub-district in Indonesia for the population healthcare need [3]. Preventive and curative service were the puskesmas’s component, integrated into primary healthcare service, financed by BPJS [3,4]. BPJS agreed to coorporate cost with the health providers referring to the Government’s tariff standards about health services cost [1,2,4]. The use of capitation payment methods may reduce healthcare expenditures due to health facilities as half or full insurer. However, inappropriate capitation rate will lead to a decrease in health services qualities [5,6]. Some studies also suggested that inexactitude of capitation rate caused by detriment of health services which was the financial risk that was more considerable than the funding of insurance providers and the lack of health facilities. [6]. Therefore, it is necessary to calculate the appropriate capitation in giving equalities to both parties [4-7].

Unit cost is the total cost incurred divided by the number of unit production including goods or services [8]. Unit cost as a primary account is required to estimate the capitation value. Before NHI era, Indonesian Dental Association/Persatuan Dokter Gigi Indonesia (PDGI) had calculated the unit cost value of dental health services using several methods such as cash basis, ABC and double-distribution method. PDGI reported that unit cost in health facilities amount to IDR 2,000 per patient. On the other hand, it has never been done after NHI era at puskesmas in Indonesia [9,10].

An appropriate methodology is very desirable to calculate the value of the health services unit cost and balancing the income and outcome according to the performance of health personnel and in accordance with the patient needs [11]. Rhys G et al., revealed that the calculation of appropriate cost service will achieve a sense of justice for health officer and patient satisfaction on the service [11]. Darmawan AS et al., claimed that conventional cost of accounting system has not been able to produce unit cost calculations accurately, and only ABC method is capable to present the cost calculation of all activities related to the product in detail [12]. The ABC method is considered as an excellent method which can provide entire and accurate information about the costs incurred to result of the product. It is a way of accumulating the total cost by tracking the cost activities that affect the outcome [13-16]. Through the ABC method it can be known how far the maximisation of health service enables healthcare providers to minimise the costs and maximise the resources, so that maximum efficiency is obtained [14-16]. Then, an advance approach used to track activities on dental health service is related to each activity based on dental healthcare pathway [14].

The geographical place also affects the dental service, and it can play a significant role in the disparity of oral health distribution services, accessibility, utilisation, treatment outcomes, oral health knowledge and practices, health insurance coverage among urban and rural communities [17]. Inequalities of healthcare services utilisation have an impact on oral health outcome and service delivery [18]. A research reported that rural dwellers have poorer oral health, limited access, and health workforce shortages than urban counterparts [19].

Based on the prior description, each production unit produces different unit cost according to the dental service pathway at puskesmas. In addition, the place of living also determines the utilisation of dental services. Therefore, the research as the first study after NHI era, aimed to compare the results of unit cost calculation of dental health services at urban and rural puskesmas in Padang City, Indonesia by using the ABC method.

Materials and Methods

Study Location and Puskesmas Profile

A quantitative descriptive study was conducted in two of 22 total Puskesmas in Padang City, West Sumatera, Indonesia. The units were classified into two groups- an urban and rural area with more than 10 dental patients per day. Puskesmas provide the primary healthcare and financed by the Indonesian government. The study was approved by The Committee of the Research Ethics, Faculty of Medicine, Andalas University (096/KEP/FK/2016). The data was collected in 2 months from April-June 2016.

Study Design

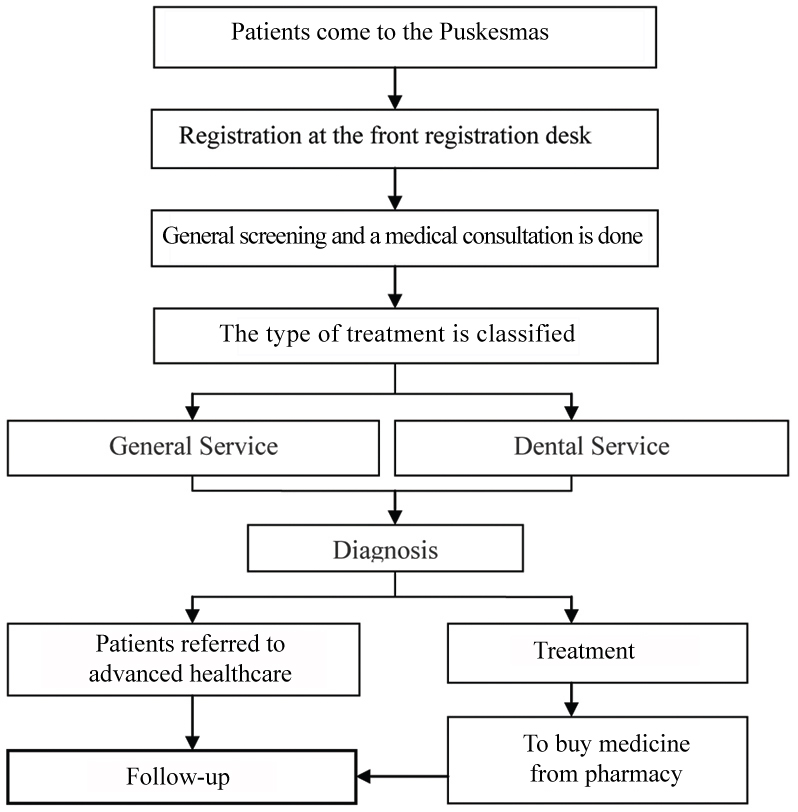

The puskesmas were selected by random sampling, one representative for urban and rural the counterpart. A retrospective database analysis was conducted to retrace the puskesmas record database between January until December 2016. Two administrative officers were interviewed to ensure the appropriateness of data at each puskesmas and complete the supplementary information. The preliminary step, was to identify the dental health service pathway [Table/Fig-1] at puskesmas based on puskesmas medical record and annual puskesmas statistical data report.

Dental health service pathway at Puskesmas.

Cost Calculation

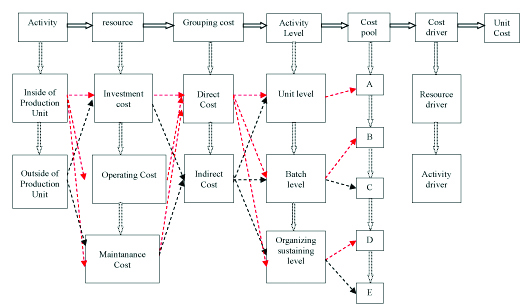

According to the purpose, Activity-Based Costing (ABC) method was used to calculate the unit cost on basic healthcare service at puskesmas [Table/Fig-2]. Firstly, identification of the dental service activities related to health workforce and the resource cost was done then grouping to the direct and indirect costs associated to dental services. Then data was classified into three activity levels, including unit level (direct activity inside dental treatment), batch level (direct activity outside the treatment), and organising-sustaining level (supportive activity). Thus, categorised each cost pool (cost group of the same activity level and cost driver) grouped by cost pool A-E based on the same activity level and cost grouping counterpart. Each cost pool A, B, C, D, E was determined by the specific grouping of level activity depending on direct or indirect cost at puskesmas. The direct group included cost pool A at the unit level (workforce costs; the cost of dental and medical consumables equipment). The indirect group consisted of cost pool B (pharmaceutical costs) and C (workforce costs) at batch level, cost pool D (routine expenditure costs) and E (workforce costs) at Organisation-Sustaining level. Total cost pool value was summarised by the whole of A, B, C, D, E cost pool. Secondly, cost driver formulated by the total cost pool divided entire patient visit per year at puskesmas Thirdly, a qualitative approach through in-deep interview was designed for the understanding of job desk per personnel, total salary and bonus. The annual mean cost per personnel resulted from total cost personnel divided by 12 months. Determination of the cost driver was used to calculate unit cost pool as changing cost factor. Cost driver using Cokins grouping was differentiated into activity driver and resource driver [20]. The last but not least was the calculation of the unit cost (total summary of unit cost pool) and expressed in the Indonesian Rupiah/Indonesia Dalam Rupiah (IDR).

Mapping of unit cost calculation using activity-based costing method on Dental Health Services.

Results

Based on this study, there were 15 officers involved in dental services in urban puskesmas, of which there were four dentists and one dental assistant. Meanwhile 12 officers consisted of three dentists and one dental assistant were directly involved in dental healthcare at rural puskesmas. [Table/Fig-3] showed that investment and maintenance costs were being excluded; only operating cost included the unit cost calculation. The rest banned due to Act No. 28 of 2014 stated that the Indonesian government is investing in the building of puskesmas at the fist, thus excluded in capitation payment method [21]. Workforce cost was the most significant number of the cost recapitulation obtained from the cost tracking results at the urban and rural puskesmas.

Cost recapitulation by usage cost groups at urban and rural Puskesmas.

| No | Fee group | Cost of puskesmas (IDR) |

|---|

| Urban | Rural |

|---|

| I | Investment costs |

| a. | Fee Means | - | - |

| b. | Infrastructure Costs | - | - |

| II | Operating costs |

| a. | Workforce costs |

| 1. | Salary | 563,108,400 | 475,516,800 |

| 2. | Bonus | 429,104,396 | 293,800,000 |

| b. | Cost of equipment and consumables |

| 1. | Dentistry | 51,481,250 | 39,210,308 |

| 2. | General | 768,250 | 1,768,750 |

| c. | Pharmaceutical costs | 11,390,924 | 12,337,351 |

| d. | Routine expenditure of puskesmas | 9,939,321 | 38,088,891 |

| III | Maintenance cost | - | - |

Level activity based on unit level, batch level, and organising-sustaining level were classified and grouped into a direct and indirect cost [Table/Fig-4]. [Table/Fig-5] demonstrates average cost charges accumulated for each cost pool. Both urban and rural puskesmas had the highest cost pool A on dental health services.

Level activity related to dental healthcare cost at urban and rural Puskesmas.

| No. | Level activity | Cost of dental service |

|---|

| Direct | Indirect |

|---|

| 1. | Unit Level | Salary and Bonus | |

| Dentistry equipment |

| General Medic |

| 2. | Batch level | Pharmaceuticals | Salary and Bonus |

| 3. | Organisation-Sustaining level | Puskesmas’s routine expenditure | Salary and Bonus |

Cost recapitulation based on cost pool at urban and rural Puskesmas.

| No. | Level activity | Cost of dental service (IDR) |

|---|

| Direct | Indirect |

|---|

| Cost pool | Urban | Rural | Cost pool | Urban | Rural |

|---|

| 1. | Unit level | A | 475,344,640 | 392,439,850 | | | |

| 2. | Batch level | B | 11,390,924 | 12,337,351 | C | 361,286,842 | 232,056,000 |

| 3. | Organising-sustaining level | D | 9,939,321 | 38,088,891 | E | 186,330,832 | 185,800,000 |

Resource drive is a ratio of total of the dental and general patient; meanwhile, activity driver is a total of the dental patient [Table/Fig-6]. The cost driver is the measurable cost change factor that included total patient, ratio health service. [Table/Fig-6] described that the urban puskesmas resource driver which was relatively (0.0306) similar to rural puskesmas (0.0348). On the other hand, urban activity driver was bigger than rural puskesmas, means urban puskesmas had more patients than the rural counterpart.

Determination of cost driver.

| Cost driver | Cost recapitulation of puskesmas |

|---|

| Urban | Rural |

|---|

| 1. | Resource Drive (ratio) | 0.0306 | 0.0348 |

| 2. | Activity Driver (total patient) | 5,814 | 3,869 |

All costs collected were divided by the cost drivers that have been specified. As the costs accumulated for cost pools A and B will be divided by the activity and accrued on the cost pool C, D and E will be multiplied by the resource driver and then shared by the activity driver. Based on [Table/Fig-7], determination of dental health services was measured by the summary of all cost pool. Cost pool A in both puskesmas was the highest among other with total unit cost pool in rural being higher than urban puskesmas.

Unit cost determination of dental health services.

| Unit cost pool | Unit cost of puskesmas |

|---|

| Urban | Rural |

|---|

| Cost pool A | 81,758.62 | 101,431.85 |

| Cost pool B | 1,1,959.22 | 3,188.76 |

| Cost pool C | 1,901.5 | 2,087.24 |

| Cost pool D | 52.3 | 342.5 |

| Cost pool E | 980.6 | 1671.19 |

| Total unit cost pool | 86,652 | 108,721 |

Cost pool A as the most significant cost pools included workforce expenditure. [Table/Fig-8] describes that the deduction of unit cost pool A and total unit cost at urban puskesmas was not differed from rural puskesmas and ranged from 5-7%. with the smallest deduction found in the urban puskesmas (4,893). The total unit value is strongly influenced by the current costs in cost pool A and impacted a small amount of other cost pool. It may be caused by investment and maintenance costs being excluded in the unit cost calculation at puskesmas.

Comparison of total cost pool and cost pool A.

| Cost pool | Unit cost (IDR) |

|---|

| Urban | Rural |

|---|

| Unit Cost pool A | 81,758 | 101,431 |

| Total Unit Cost Pool | 86,652 | 108,721 |

| Deduction | 4,894 (5.64%) | 7,289 (6.70%) |

Cost pool A being directly involved in dental services, consisted of workforce cost, equipment, and dental consumables cost, and general medical consumables for dental services cost. [Table/Fig-9] showed that the workforce cost is the largest cost of cost pool A. Only about 10% is used for others including equipment and dental consumables, and general medical consumables in urban and rural puskesmas.

Comparison of cost driver at Puskesmas.

| Cost pool | Puskesmas |

|---|

| Urban | Rural |

|---|

| Total Cost Pool A | 475,344,640 | 392,439,850 |

| Total Sallary and bonus | 423,095,140 | 351,460,792 |

| Difference | 52,249,500 | 40,979,058 |

| % Difference | 10.99% | 10.44% |

[Table/Fig-10] demonstrated that the average cost per year for dental health services at rural and urban puskesmas almost similar and ranged from 84 to 88 million/year. Meanwhile, the dental caretaker cost in rural (IDR 90,840/service) was higher than urban counterpart (IDR 72,771/service).

Comparison of total cost and unit cost of dental caretaker.

| Cost pool | Primary health center |

|---|

| Urban | Rural |

|---|

| Total personnel | 5 | 4 |

| Service activity | 5,814 | 3,869 |

| Jobdesk per personnel | 1,162 | 967 |

| Total Cost Personnel (IDR) | 423,095,140 | 351,460,792 |

| Mean Cost per personnel/years (IDR) | 84,619,028 | 87,865,198 |

| Unit cost per service (IDR) | 72,771 | 90,840 |

Discussion

The evolution of Indonesian Healthcare System might be unique. Since the reformation of the NHI era, the Indonesian government has launched universal health insurance managed by BPJS. The funding was delivered to the primary healthcare (puskesmas and Pratama clinic) and advance healthcare (hospital). Puskesmas were established to improve the integrative program of preventive and curative healthcare. The funding of basic healthcare service financed by the Indonesian government is only allocated for operational costs and services. Meanwhile, investment and maintenance costs are excluded, so it is only considerate for the operating cost on cost recapitulation by cost usage [Table/Fig-3] [1,2,4]. Furthermore, we calculated the unit cost of dental health service based on capitation method in general and not per case. This result has a significant difference with Vo TQ et al., in Vietnam that analysed estimating cost resource from one case then calculated the cost based on the resource utilisation [20].

By using the ABC methods, we could evaluate the most significant cost value for dental service; it gives a lot of information about the dental health services-unit cost value of each primary health care and provide the detailed cost of one service to each activity after NHI era. The result revealed that the unit cost of dental service in urban puskesmas was IDR 86.652 and rural was IDR 108,721 with the total mean of the unit cost at puskesmas being IDR 97,686. Unit cost calculation by Indonesian Dental Association study before NHI era covered by Indonesian insurance was IDR 98.404 and estimation of Indonesian government calculation was IDR 98.522. Both of the calculation result are in range with our study result. Therefore, the result of this study was accurate and gave a detailed explanation of primary health care at puskesmas in the urban and rural area. Hence, our research could help the Government to analyse the kind of cost in primary health care that impacted the unit cost after the NHI era [9,10].

This study showed that there was a average difference of dental health service-unit cost between urban (IDR 86,652) and rural (IDR 108,721,63) due to the unequal distribution of the total officers at each puskesmas. According to the result, the highest cost value for a dental service comes from dental health personnel cost with low income from dental health service at puskesmas in a year. Viewed from mean cost per person per years, rural puskesmas (IDR 87,865,198) spend more cost than urban puskesmas (IDR 84,619,028). Based on the job desk per personnel, urban puskesmas had a higher workload than rural puskesmas. It means that rural puskesmas spend more money on one activity of one dental officer than urban puskesmas. This disparity can be explained mainly by the inexactitude distribution of dental caretaker, as well as inequitable and inadequate access to oral healthcare services in the rural and urban area [17-19].

Limitation

This finding has some restraint that should be lightly interpretated that average cost only concentrated on cost calculation per type of treatment not per case due to capitation method, by the Indonesian government. Furthermore, each activity was independently gathered with general and medical health services, so all the dental services must be specifically stratified. Besides, the result of the annual unit cost calculation will be different according to each activity per year.

Conclusion

Unit cost calculation based on ABC method can help the decision makers to provide accurate and precise information about improving the efficiency and effectiveness of each officer’ workload and designing strategies that could be implemented to improve the quality of dental healthcare service. The result of this study also helps the Indonesian government to determine the reasonable Indonesian capitation value.

Abbreviations

NHI National Health Insurance; BPJS Badan Penyelenggara Jaminan Sosial/Social Security Administering Board; PUSKESMAS Community-based health service; PDGI Persatuan Dokter Gigi Indonesia/Indonesian Dental Association; ABC Activity Based Costing; IDR Indonesia Dalam Rupiah/Indonesian Rupiah.

Disclosure

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and or publication of this article.

[1]. Pemerintah RI. Undang-Undang Republik Indonesia Nomor 40 Tahun 2004 tentang Sistem Jaminan Kesehatan Nasional. 2004. Available at: https://jdih.kemenkeu.go.id/fulltext/2004/40TAHUN2004UU.htm [Google Scholar]

[2]. Kemenkes RI, Penggunaan Dana Kapitasi Jaminan Kesehatan Nasional Untuk Jasa Pelayanan Kesehatan dan Dukungan Biaya Operasional Pada Fasilitas Kesehatan Tingkat Pertama Milik Pemerintah Daerah 2014 JakartaKemenkes RIAvailable at: http://sinforeg.litbang.depkes.go.id/upload/regulasi/PMK_No._19_ttg_Penggunaan_Dana_Kapitasi_Jaminan_Kesehatan_.pdf [Google Scholar]

[3]. Suryanto , Plummer V, Boyle M, Healthcare System in IndonesiaHospital Topics 2017 95(4):82-89.10.1080/00185868.2017.133380628636456 [Google Scholar] [CrossRef] [PubMed]

[4]. Andoh-Adjei FX, van der Wal R, Nsiah-Boateng E, Asante FA, van der Velden K, Spaan E, Does capitation payment under national health insurance affect subscriber’s trust in their primary care provider? a cross-sectional survey of insurance subscribers in GhanaBMC Health Serv Res 2018 18(1):5210.1186/s12913-018-2859-629378567 [Google Scholar] [CrossRef] [PubMed]

[5]. Andoh-Adjei F, Wal R, Nsiah-Boateng E, Asante FA, Velden K, Spaan E, Does a provider payment affect membership retention in a health insurance schemes? a mixed method Study of Ghana’s capitation payment for Primary CareBMC Health Services Research 2018 18(52):1-11.10.1186/s12913-018-2859-629378567 [Google Scholar] [CrossRef] [PubMed]

[6]. Vo TQ, Tran HTT, Nguyen NP, Nguyen HTS, Ha TV, Le NQ, Economic aspects of post-stroke rehabilitation: a retrospective data at a traditional medicine hospital in VietnamJournal of Clinical and Diagnostic Research 2018 12(6):5-10.10.7860/JCDR/2018/35730.11578 [Google Scholar] [CrossRef]

[7]. Horngren CT, Datar SM, Rajan MV, Cost Accounting: A Managerial Emphasis, England, Pearson 2012 [Google Scholar]

[8]. PDGI 2013. Pelayanan Primer dan Gatekeeper Bidang Kedokteran Gigi, Jakarta, PDGI [Google Scholar]

[9]. PB IDI, 2013. Metode Membayar Dokter Layanan Primer Dalam Era JKN, Jakarta, IDI. Available at: http://www.idionline.org/wp-content/uploads/2015/01/metode-membayar-dlp-di-era-jkn-7-okt-2013-ngs-final-1.compressed.pdf [Google Scholar]

[10]. Popesko B, Specifics of the Activity-Based Costing applications in Hospital ManagementInt J Collab Res Intern Med Public Health 2013 5(3)):179-86. [Google Scholar]

[11]. Rhys G, Beerstecher HJ, Morgan CL, Primary Care Capitation Payments in the UK. An Observational StudyBMC Health Services Research 2010 10:15610.1186/1472-6963-10-15620529330 [Google Scholar] [CrossRef] [PubMed]

[12]. Darmawan AS, Tingkat Keakuratan Penentuan Biaya Produksi Jurnal Ilmiah Akutansi dan Humanika 2011 Available at: http://ejournal.undiksha.ac.id/index.php/JJA/article/view/300/255 [Google Scholar]

[13]. Javid M, Hadian M, Ghaderi H, Ghaffari S, Salehi M, Application of the activity-based costing method for unit-cost calculation in a HospitalGlob J Health Sci 2015 8(1):165-72.10.5539/gjhs.v8n1p16526234974 [Google Scholar] [CrossRef] [PubMed]

[14]. Garrison RH, Noreen EW, dan Brewer PC, 2008. Managerial Accounting, Jakarta, Salemba Empat 2010 Thirteenth EditionNew York, NYMcGraw Hill/Irwin:xxxi:804Available at: https://www.aaajournals.org/doi/pdf/10.2308/iace.2010.25.4.792 [Google Scholar]

[15]. Than TM, Saw YM, Khaing M, Win EI, Cho SM, Kariya T, Unit cost of healthcare services at 200-bed public hospitals in Myanmar: what plays an important role of hospital budgeting?BMC Health Serv Res 2017 17(669):1-12.10.1186/s12913-017-2619-z28927450 [Google Scholar] [CrossRef] [PubMed]

[16]. Ogunbodede E, Kida I, Madjapa H, Amedari M, Ehizele A, Mutave R, Oral health inequalities between rural and urban populations of the African and Middle East regionAdv Dent Res 2015 27(1):18-25.10.1177/002203451557553826101336 [Google Scholar] [CrossRef] [PubMed]

[17]. Gaber A, Galarneau C, Feine JS, Emami E, Rural-urban disparity in oral health-related quality of lifeCommunity Dent Oral Epidemiol 2018 46(2):132-142.10.1111/cdoe.1234428940682 [Google Scholar] [CrossRef] [PubMed]

[18]. Barnett T, Hoang Ha, Stuart J, Crocombe L, The relationship of primary care providers to dental practitioner in rural and remote AustraliaBMC Health Serv Res 2017 17:1-13.10.1186/s12913-017-2473-z28764806 [Google Scholar] [CrossRef] [PubMed]

[19]. Cokins G, Implementing Activity-Based CostingInstitute of Management Accountants 2006 Available from: https://www.imanet.org/-/media/975e063f2e4a4734823b99864ec58bb5.ashx?as=1&mh=200&mw=200&hash=B35D86547A7A67D6D15F6649BEA6A77D76A261CD [Google Scholar]

[20]. Vo TQ, Tran HTT, Nguyen TD, Tran QV, Pham SNX, Economic analysis of hospitalised paediatric community-acquired-pneumonia at a private hospital in southern Vietnam, Fiscal Year 2015-2016J Clin Diagn Res 2018 12(6):LC11-LC15.10.7860/JCDR/2018/35732.11579 [Google Scholar] [CrossRef]

[21]. Pemerintah RI. Peraturan Menteri Kesehatan Republik Indonesia Nomor 28 Tahun 2014 tentang Kapitasi. 2014. Available at: https://www.kemhan.go.id/itjen/wp-content/uploads/2017/03/bn874-2014.pdf [Google Scholar]